1

181962

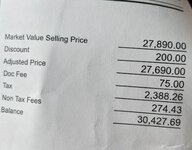

If the deal was borrowing more at 0% with no offsetting consideration it's pretty much best to borrow more for just about anybody and put the money in savings. Even if somebody is living hand to mouth and wants to keep the monthly payment down, the money kept in savings could make up the difference providing they didn't spend it on something else.I put 20% down (financed the rest at 0%).

In wondering if I might have been better trying to put less down. If I have an accident now, My car is worth either what I financed it for, or maybe a little more. My insurance will give me the cash value (prior to it getting totaled), plus up to 20 or 25% ... something like that, if needed to pay off the loan.

But since my loan is close to the cash value of the car, that’s all I’ll get.

I’ll loose my down payment entirely.

I’d have been much better off putting less down, and just sticking the cash instead in a savings or investing it. Then, if my car got totaled, I’d still be able to replace my car with a brand new one of the same type.

Stupid advice, “put 20% down”, I think. Sigh.

I wouldn't beat yourself up too much. If you put that extra down in a conservative investment, something with guaranteed or reasonable assurance it would not lose principal in the event you need to draw on it in an emergency like a savings account or money market fund, the earnings on those accounts are near 0% anyway (and will be there for some time to come) unless you find a teaser rate on a new account that might not last very long. As an emergency fund, you would surely not want to put it in the stock market since it may not all be there when you need it.

Even if you could find an account that would pay you 2% compounded interest for the next 5 years, and it is liquid and not a CD where you'd forfeit interest if you had to draw on it, and the down payment was 10% on $35,000 vehicle instead of 20%, the earnings over 5 years on the $3,500 in savings would be about $942, or about $16 per week if you want to look at it that way. At more typical 0.10% interest that's a whomping $18 in earnings over 5 years or $0.30 per week.

What maybe doesn't make much sense is putting 20% down and paying extra for gap insurance. With that amount down, expecially with a reasonable amount off MSRP in the purchase price, you should never be underwater on a 5 year loan. The larger down payment means your net after a total is that much larger. If you totaled a 2020 today you'll end up with some cash in your pocket after insurance pays off the loan.

Further, while it's true that a car loses 15% of its value when you drive it off the lot, that's from the perspective of trade value. A decent insurance company will pay out what it costs you to replace that vehicle in kind including the sales tax. You might be surprised at what the insurance company might pay in a total. My wife totaled a $31,000 all-in vehicle including tax and whatnot that was $4,500 off MSRP with a 0% loan after 5 months and and less than 5,000 miles. The insurance payout was only $1,000 less than what I paid, and that was after a $500 deductible, so the depreciation was only $500.

At this juncture I would look into cancelling the gap insurance. If that's a line item in an auto insurance policy you could see what you're paying for it. I would also check reviews of the claim service of your auto carrier. If they are average or above you'll likely get a reasonable payout in a total.

Last edited by a moderator:

")